| https://www.next-finance.net/en | |

|

Opinion

|

Reasons to embrace risk

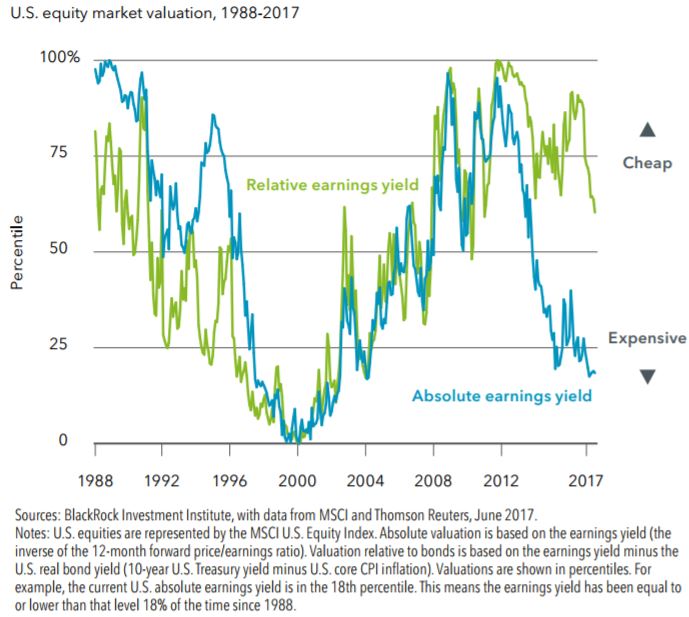

According to Richard Turnill, BlackRock’s Global Chief Investment Strategist, if we look at the earnings yield of U.S. equities — the implied yield in earnings estimates that makes potential returns comparable to bond yields. U.S. equities look expensive on this basis. But compared with historically low bond yields, U.S. equities still look cheap.

The global economy is chugging along, with the eurozone perking up even as inflation remains subdued. In a low-yield environment, we believe this bodes well for risk assets.

We look at the earnings yield of U.S. equities — the implied yield in earnings estimates that makes potential returns comparable to bond yields. U.S. equities look expensive on this basis, as shown by the blue line in the chart. But compared with historically low bond yields (green line), U.S. equities still look cheap.

Rethinking returns

We see the world in a synchronized and sustained economic expansion, as detailed in our Global investment outlook: Midyear 2017 . Eurozone’s growth has accelerated, and we believe any near-term worries on China are likely overstated. Yet overall we see an environment of structurally lower growth and interest rates. This suggests comparing today’s valuation metrics to past levels may not be as useful of a guide to future returns as in previous cycles.

The current U.S. economic cycle has been unusually long, sparking fears that it is ready to die of old age. We compared this cycle with previous ones, based on estimates of economic slack, and found it has room to run. One consequence: A benign economic environment tends to go hand in hand with low market volatility. We see risks of policy missteps as the Federal Reserve plans to wind down its balance sheet and the European Central Bank looks to transition towards smaller asset purchases. A sharp rise in bond yields could undercut risk assets, but we expect both central banks will communicate clearly and proceed with caution.

Bottom line: We believe investors are being paid to take risk, and prefer equities over fixed income. We like European, Japanese and emerging market shares, as well as the momentum factor. We are negative on major government bonds and prefer inflation-linked debt.

Richard Turnill , July 2017

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |