Nearing the end of a ‘junk rally’?

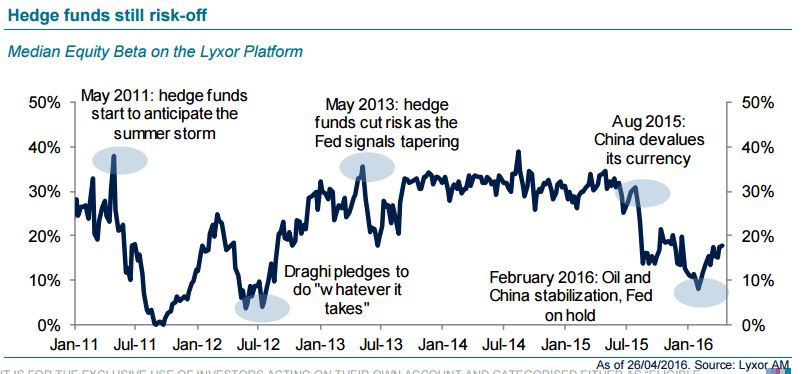

Hedge funds’ returns weakened in sympathy with last week’s retreat in risky assets. Losses were mild in general, with few notable underperformers. By contrast, CTAs outperformed, recouping their earlier losses as yields and oil weakened. Funds keeping a low beta also performed well, the neutral and variable equity funds especially.

Article also available in :

English ![]() |

français

|

français ![]()

Hedge funds’ returns weakened in sympathy with last week’s retreat in risky assets. Losses were mild in general, with few notable underperformers. By contrast, CTAs outperformed, recouping their earlier losses as yields and oil weakened. Funds keeping a low beta also performed well, the neutral and variable equity funds especially.

Sentiment deteriorated last week. A number of mixed economic releases failed to demonstrate any pick up in fundamentals. Macro data remained consistent with a sluggish global growth environment neither gaining nor losing momentum.

The environment since the rally started by mid-February was particularly uncomfortable for most asset managers. A binary macro backdrop and rich valuations maintained high uncertainties, preventing most investors from taking aggressive bets.

The rally largely reflected renewed optimism on China and the global recovery, whilst the Fed was priced to remain on hold. We believe that these stances are vulnerable.

Monetary policies remain pivotal for many assets, that of the Fed especially. Central banks’ meeting, minutes and comments are fuelling frequent asset rotations, which are difficult to arbitrage. This was yet again illustrated by the latest BoJ disappointment.

In that context, most asset managers (traditional and alternative alike) were reluctant to join in the rally and remained cautious. As a result funds’ returns are looking increasingly pale compared to major market indices. Managers are likely to feel a growing pressure on alpha generation.

We are keeping a slight overweight on CTAs. The environment is mixed but trend followers provide a hedge against volatility and a source of diversification.

We currently find the greatest alpha potential in the Merger arbitrage, in the variable bias L/S Equity and in the Credit funds.

Lyxor Research , May 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

News Institutional investor appetite is back for quant funds

The recent CTA performances encourage institutional investors to more closely monitor this type of hedge fund. Thus, according to Preqin, 52% of them wish to increase their exposure to this type of alternative strategy this year (vs 14% last (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |