| https://www.next-finance.net/en | |

|

Strategy

|

Gold & Mines – A good way to diversify in the current environment!

According to Arnaud du Plessis, CPR AM thematic equities manager specialising in gold and commodities, after the US Nonfarm Payrolls fell far short of expectations in early June, a further boost to the gold market was provided by the Brexit vote. The big winners are UK investors who had the bright idea of converting their savings into gold...

Article also available in :

English ![]() |

français

|

français ![]()

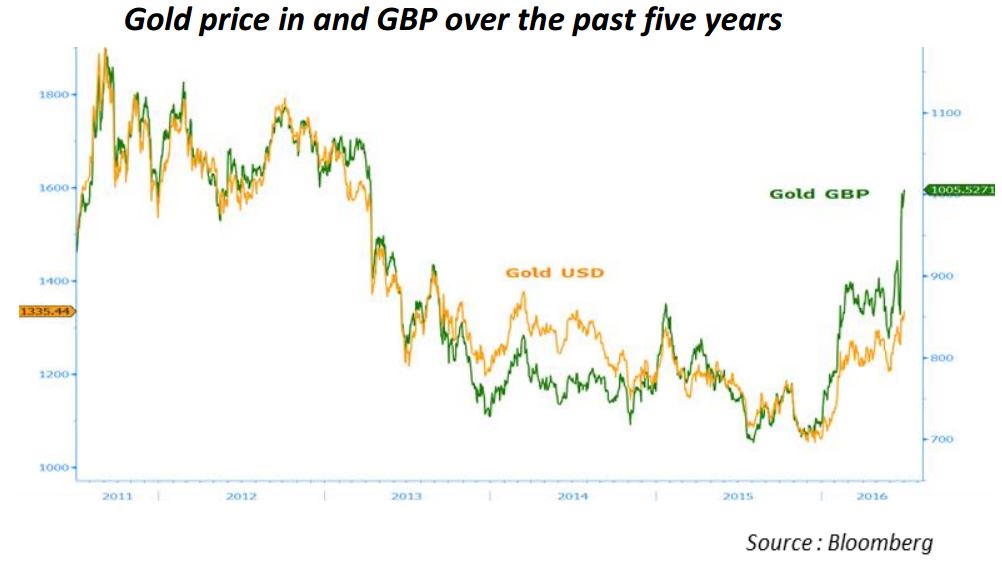

After the US Nonfarm Payrolls fell far short of expectations in early June, a further boost to the gold market was provided by the Brexit vote. The big winners are UK investors who had the bright idea of converting their savings into gold on the day before the outcome was announced. Gold brushed up against the £1000 barrier, a level last reached in April 2013. This was far ahead of the price in dollar terms, which returned “only” as far as its March 2014 level at $1359/oz., before dipping somewhat late in the month.

With a potential Brexit now on the table, the market has effectively priced out the possibility of a Fed rate hike in 2016 and even 2017. This has provided a further boost to gold, which is extremely sensitive to this indicator. Sovereign yields’ further move into negative territory worldwide is a second highly positive factor.

However, gold has diverged widely from trends in its other key markets, such as the US dollar, inflation expectations, and, to a lesser extent, real US interest rates. Market turmoil in recent days is obviously the cause of this, and a lull would probably lead to a consolidation of the gold market.

Meanwhile, investors remain keen on ETPs backed by physical gold. Another 100 tonne-plus equivalent was stockpiled in June, raising the increase in stocks to almost 500 tonnes on the year to date, a level not seen since September 2013.

The same trend was seen on the futures market, with non-commercial long positions setting a new record at 371k lots (i.e., 37.1m oz. or 1154 tonnes), vs. net positions of 317K lots (31.7m oz. or 986 tonnes). So the market is clearly long gold – a contrarian indicator to be watched closely, especially as central banks are slowing their purchases, the People’s Bank of China included. Things are different for the large “consumers” – the Chinese and Indians. While Chinese imports, via Hong Kong, surged by 68% (MoM) in May to 115 tonnes, for a total of 342 tonnes on the year to date (+3% YoY), Indian purchases were sluggish, hit by higher prices and falling 53% (YTD to end-May) vs. the same period of 2015. So caution is in order, even though the environment remains very favourable to gold.

AuM (contracts) on future markets (CFTC) and gold ETPs and gold price ($/oz. since 2009)

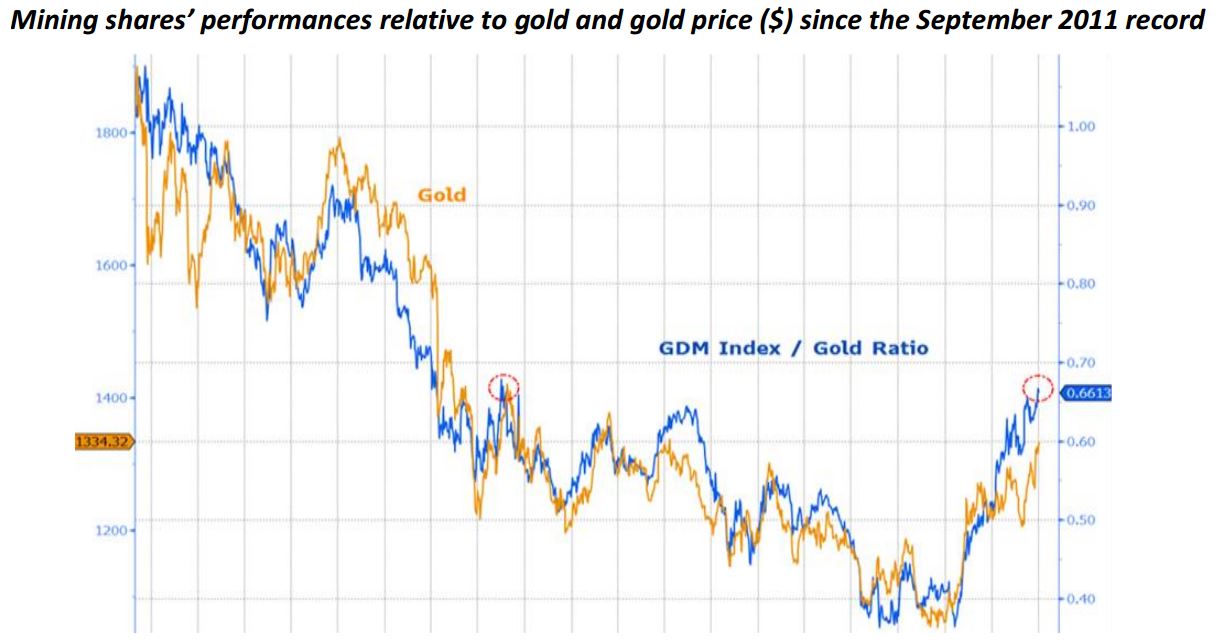

As for mining shares, they have never fared so well over a half-year period! Rising more than 100% ($), they offered leverage of about 4x vs. gold, significantly higher than the long-term average (about 2x). The most heavily leveraged mines, which were distressed late last year, rallied the most, with some of them up almost +300% on the year to date! Higher gold prices, along with lower costs, have provided a big boost to margins, which may improve by more than 75% in 2016, assuming an average gold price of about $1300/oz.

Goldmines: All-In Sustaining Costs (AISC), All-In Margin and Gold Price since 2004

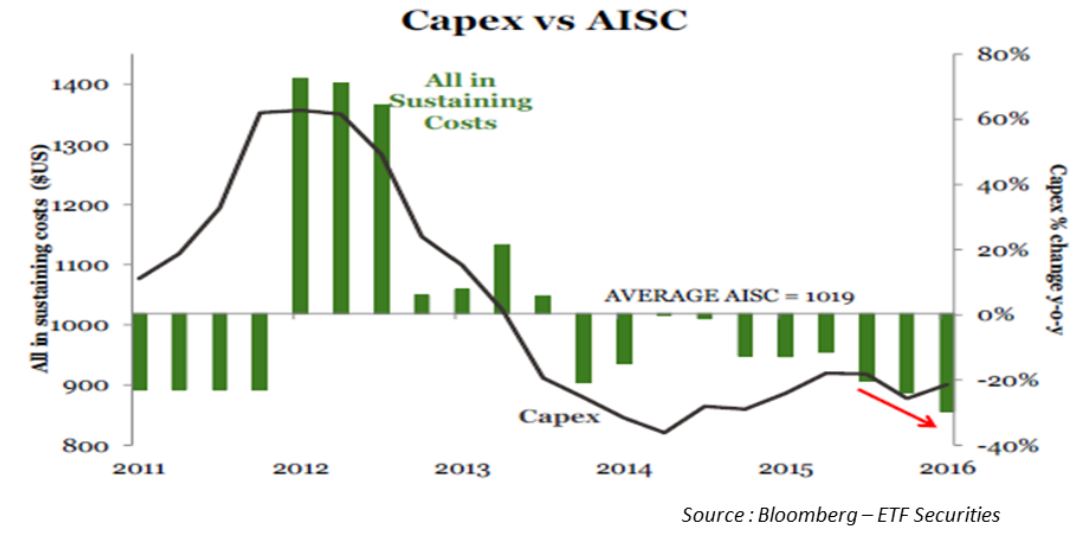

It is worth pointing out that a significant portion of lower costs (AISC) is due to lower capital expenditure. This has helped considerably lower the industry’s debt levels, a lurking threat if the gold price had continued to fall. However, lower capex will have a clear impact on future output, which may decline even more rapidly. Mining companies will be unable to maintain this pace for very long in these conditions. Barring new projects, whose complexity has risen constantly in recent years, the major mining groups will have to make acquisitions to keep up their output.

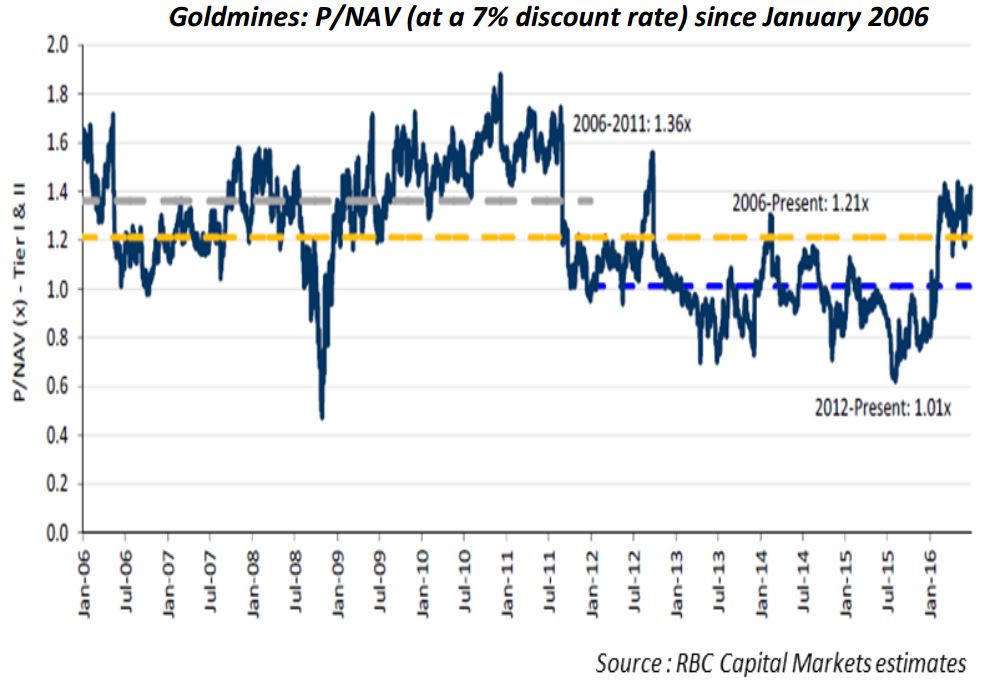

After this run-up, mining shares discount vs. gold has clearly receded. At a P/NAV of about 1.4x/1.5x, they have already priced in a further improvement in the gold price. The release of quarterly results and, even more so, company guidance will be key to what happens next.

Goldmines have outperformed gold by far since bottoming out last year. They have returned to their relative level of August 2013 when gold prices were around $1400/oz. The trend is in the right direction but much has already been priced in. Note that in the first half of this year gold averaged just $1219/oz., vs. $1205/oz. in the first half of 2015. The consensus remains highly conservative, averaging just $1225/oz. for the full year. Mining stocks are already pricing in a gold price of at least $1300/oz.

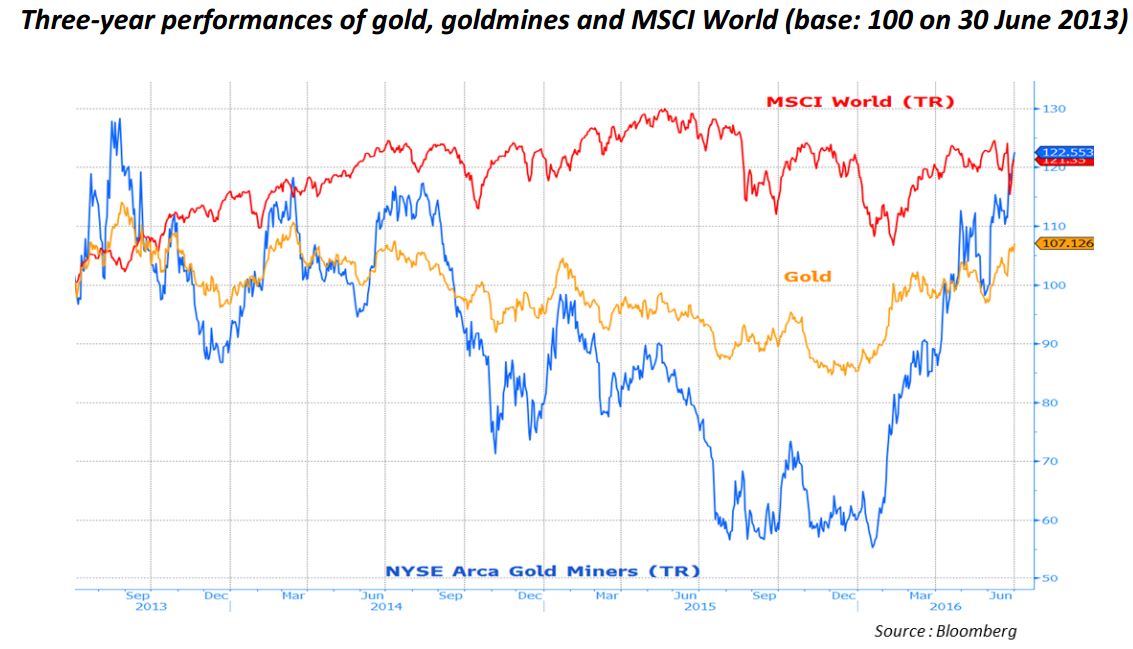

In the meantime, goldmines are playing their portfolio diversification role to the hilt. The sector (as measured by the NYSE Arca Gold Miners Index) is now vastly outperforming global equities (the MSCI World) over the past two years, at +7.95% ($) vs. -2.2% ($) and is performing as strongly over the past three years, at +22.5% ($) vs +21.3% ($).

Arnaud du Plessis , July 2016

Article also available in :

English ![]() |

français

|

français ![]()

Focus

Strategy CPR AM has recently launched CPR Invest – Global Disruptive Opportunities | A look back at an accelerating phenomenon: disruption

The recently theorised phenomenon of "disruption" is defined as a process whereby a product, a service or a solution disrupts the rules on an already established market. Technological progress, along with the globalisation of trade and demographic changes are now helping to (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |