| https://www.next-finance.net/en | |

|

Opinion

|

French elections – Place your bets, last call

While a moderate candidate is the most likely victor in our assessment, the situation remains fluid with little risk priced in. In such an environment, we believe it is important to protect investors in our multi asset portfolios from market shocks. We have tactically reduced exposure to financial markets and increased exposure to the Japanese yen for its defensive qualities in times of stress.

As we approach the first round of the French presidential elections on 23rd April, the uncertainty over who will make it into round two, and the final result, has never been greater.

While a moderate candidate is the most likely victor in our assessment, the situation remains fluid with little risk priced in. In such an environment, we believe it is important to protect investors in our multi asset portfolios from market shocks. We have tactically reduced exposure to financial markets and increased exposure to the Japanese yen for its defensive qualities in times of stress.

The paradox of choice?

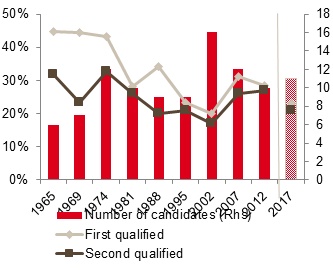

One factor behind the uncertainty is choice. Not only is the number of candidates in the first round of the election higher than average (11 versus a low of six in 1965 and a high of 16 in 2002), the situation could repeat itself in the second round.

The polls currently suggest that four candidates are likely to make it through to round two (Emmanuel Macron, Marine Le Pen, François Fillon and Jean-Luc Mélenchon) compared with two or three for previous elections. This creates a risk of surprise because it substantially lowers the vote required to make it to the second round. In the past nine presidential elections, a 25% share of the vote was required to make it to round two. As can be seen from the chart below, we estimate the required threshold for 2017 to be as low as 20-21%.

If the votes are close, a wide field in the second round increases the likelihood of a surprise outcome.

French presidential elections: candidates and thresholds

- Source: Unigestion calculations, Unigestion estimates for 2017, as at April 2017.

Deciding to abstain. Possibly.

Contributing to the risk of a surprise outcome is the continuing disillusionment and indecision of French voters in an election marked by scandals and party in-fighting. According to the latest Ifop/Fiducial survey, the abstention rate could be as high as 35%, considerably ahead of the previous record of 28% in 2012. The average has been 20% since 1965.

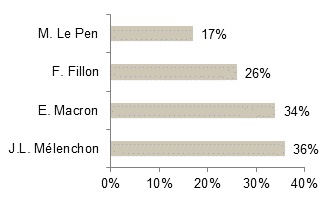

More than that, a significant number of voters have declared themselves likely to change their vote. A third of the potential voters of M. Mélenchon and M. Macron are still unsure of their final choice. This falls to 26% for electors of M. Fillon and to 17% for the supporters of Mme Le Pen.

Share of supporters likely to change candidates

- Source: Ifop-Fiducial, Unigestion calculations. April 2017.

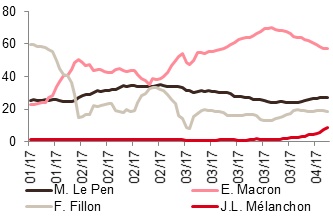

Daily tracker for first-round voting, weighted by certainty

- Source: Ifop/Fiducial, Unigestion calculations. Daily tracker. April 2017

Weighing the probabilities

While the most likely scenario is the victory of a moderate M. Macron or M. Fillon, as asset managers we believe it is important to assess the full nature of the risks, consider the extent to which they are already priced in by financial markets, and position our clients’ portfolios accordingly.

A review of the implied probabilities of each candidate calculated by Oddschecker.com, based on bookmakers’ bets, points out that the “pricing” of left-wing candidate M. Mélenchon does not reflect the recent surge in his polling (or indeed for Mme. Le Pen the recent weakness in her polling).

Implied probability to win the French election

- Sources: Oddschecker.com, Unigestion. April 2017.

Is this priced into markets? The risk premium attached to French government bonds over German is 70 basis points, far from 2011’s 190 bps. The negative skew in European options markets and volatility in the euro/dollar show some defensive positioning, but we believe little risk is priced in.

Protecting performance

After a strong first quarter, supported by a clear improvement in the macroeconomic environment, we believe that a victory for one of the populist candidates, or even a higher than expected poll showing, could prompt profit-taking or more defensive positioning by investors. For us, the balance between likely risk and return has shifted unfavourably.

As a result, we are acting now to protect the performance delivered in the first three months of the year and safeguard against the risk of a major surprise during the French presidential election. While unlikely, the risks are real and we believe this scenario is currently underestimated by investors.

We are significantly reducing our exposure to risk premia and increasing our cash position for the multi asset strategies we manage. In parallel, we are increasing our currency position in favor of the yen. Finally, in order to limit the opportunity cost of this protection strategy, we are implementing options strategies on European assets (call buying) to benefit from the asymmetry between the implied volatility of puts and calls.

This global risk strategy was successfully implemented in 2016 during the Brexit and US elections. These events also taught us that: 1) polls can be misleading and 2) it was important to remain flexible and stand ready to act quickly in the event of positive results.

Unigestion , April 2017

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |