| https://www.next-finance.net/en | |

|

Opinion

|

Combining Active and Passive management in a Portfolio

In recent years, long-held ideas on portfolio construction have been called into question. Investors can now choose from a range of “smart beta” strategies, offering exposure to market risk premia in a systematic, transparent fashion. Where does the dividing line between active and passive fund management now lie? What is the likely future role of active managers?

Article also available in :

English ![]() |

français

|

français ![]()

In recent years, long-held ideas on portfolio construction have been called into question. Investors can now choose from a range of “smart beta” strategies, offering exposure to market risk premia in a systematic, transparent fashion. Where does the dividing line between active and passive fund management now lie? What is the likely future role of active managers? And as indices evolve, how should standard, capitalisation-weighted benchmarks be used? In this Expert Opinion, Nicolas Gaussel, Chief Investment Officer at Lyxor Asset Management and Arnaud Llinas, Lyxor’s Head of ETFs and Indexing, share their views on these important questions.

TRADITIONAL “CORE” ACTIVE MANAGEMENT IS SHRINKING

[Nicolas Gaussel] One trend that has dominated asset management since the turn of the millennium is the shift of assets away from traditional “core” active mandates.

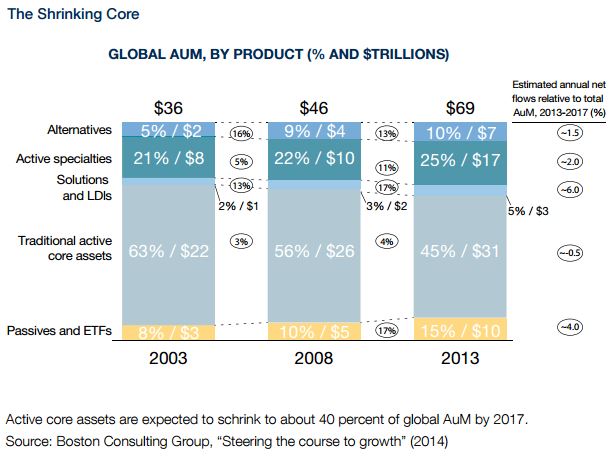

According to a 2014 study by Boston Consulting Group (BCG), active core assets represented 63% of global assets under management in 2003, but this figure is likely to fall to 40% by 2017. Investors worldwide have been moving away from traditional active management into alternatives, dedicated active mandates, solutions and liability-driven investment (LDI) schemes. There is also a big rise of passive funds in allocations, including exchangetraded funds (ETFs).

So we are witnessing a bipolarisation of the asset management market: increased demand for specialist active management, on the one hand, and for passive mandates on the other. Traditional active managers are under increasing pressure to justify their roles.

PASSIVE FUNDS ARE GROWING

[Arnaud Llinas] In its study, BCG noted that passive mandates and ETFs had grown from $3 trillion to $10 trillion in assets under management between 2003 and 2013, and BCG expects this market segment to continue to grow healthily. We think there are four reasons for this trend.

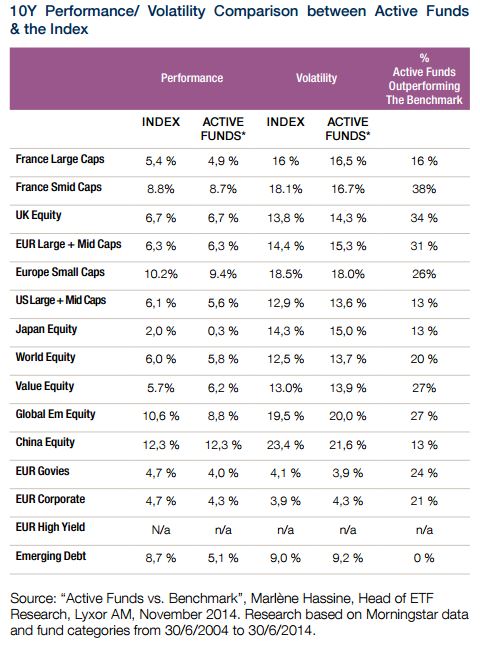

First, active managers continue to underperform their benchmarks in aggregate. According to a recently published study by my colleague Marlène Hassine, Lyxor’s Head of ETF Research, only 21% of active funds on average outperformed their benchmark over the last 10 years. And the evidence also shows that there is little persistency in performance over time. Managers that beat the benchmark in one year have thus a poor chance of doing the same the next year.

Second, passive funds, including ETFs, have a clear cost advantage against active funds, leading many investors to decide that they would prefer to track an index rather than to try and beat it. Of course, it’s fair to point out that passive funds don’t replicate their indices exactly. Other things being equal, they will trail it by their annual costs of management. However, passive funds’ costs are relatively low and have been steadily decreasing.

Third, passive funds now offer access to a broad range of asset classes and with a great degree of granularity, offering investors significant choice. Passive funds are typically highly diversified, giving wide access to individual market segments.

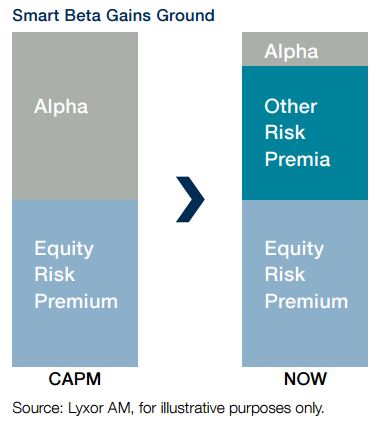

Fourth, smart beta—investment strategies, codified as indices, with an ease of replication in a systematic, transparent method—is an increasingly important phenomenon.

SMART BETA EXPANDS THE DEFINITION OF PASSIVE

[A.L.] Smart beta is expanding the traditional definition of passive investing, and in a way that offers investors a valuable new tool. Various types of portfolio strategy traditionally undertaken by active investment managers can now be replicated efficiently and at low cost via smart beta indices. In other words, passive funds are increasingly being used to give exposure to strategies that were historically offered only in an active format. To some extent, smart beta is also likely to replace some of investors’ traditional allocation to passive funds, tracking indices weighted by market capitalisation.

In a recent Expert Opinion from Lyxor [1], my colleague Thierry Roncalli, Lyxor’s Director of Research provided an overview of the concept of risk factors. Risk factors help us understand the performance of equities and other asset classes, and an increasing number of smart beta indices offer exposure to individual risk factors.

There are other popular types of smart beta index, including those focusing on the reweighting of index constituents, on particular investment styles or on specific risk outcomes, such as minimising volatility.

In the future, we think that many portfolios will include an important allocation to smart beta, as well as to traditional beta and to active management alpha.

ALTERNATIVES OFFER UNCORRELATED RISK PREMIA

[N.G.] It may seem paradoxical that the demand for alternative asset management structures, such as hedge funds, has been increasing in the midst of this boom for indexing and passive solutions.

But investor inflows into alternatives have been very strong. BCG estimated in 2014 that alternative assets more than trebled between 2003 and 2013. Another study, conducted by Cliffwater and Lyxor, found that the weighting of alternatives in US state pension funds has recently more than doubled, rising from 10% in 2006 to 24% in 2013 [2].

During a period of great volatility in asset markets and despite the negative headlines associated with some hedge funds, investors continue to be attracted by alternatives’ ability to generate attractive risk-adjusted returns.

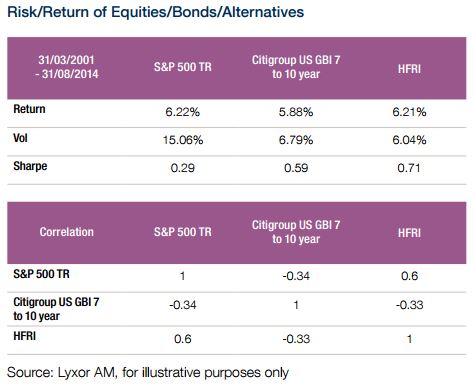

Over the period between 2001 and 2014 US equities (the S&P 500 index) and US government bonds (the Citigroup US GB 7-10 year index) and hedge funds (in the form of the HFRI index) all gave total returns of around 6% a year. But while US equities had annual volatility of around 15% over the period, hedge funds had bond-like volatility of around 6%. Hedge fund returns were also negatively correlated to bond returns, and only weakly correlated to those of equities.

These statistics reinforce the central attraction of alternatives: they can act as an effective portfolio diversifier, offering uncorrelated risk premia. And this results from hedge funds’ exposure to non-traditional asset classes.

ALTERNATIVES AS TRUE ACTIVE MANAGEMENT

[N.G.] Increasingly, alternatives are being seen as the true home of active asset management. Hedge funds are often relatively unconstrained in the investment positions they are allowed to take. By contrast, in many traditional core active management mandates performance is measured relative to an index benchmark, and managers may be reluctant to depart too far from index weightings. The difference between traditional active mandates and hedge funds is also supported by a lot of academic research. For example, in 2009 Professors Ang, Goetzmann and Schaefer reviewed the performance of the active management of the Norwegian Government Pension Fund, which was largely based on traditional mandates [3].

The researchers concluded that a significant proportion of the fund’s historical returns could be explained by exposure to systematic risk factors, rather than occurring as a result of active manager skill. This takes me back to Arnaud’s point about smart beta: it’s increasingly possible to access these risk factors via transparent and low-cost index solutions, rather than paying extra to access them via active mandates.

In another study, published in 2012 and focusing on the period from 1990-2008 [4], academics Aglietta, Brière, Rigot and Signori showed that active management had contributed nothing to US pension funds’ returns within the equity asset class and very little to the funds’ returns in fixed income.

In fact, most of the equity and fixed income returns earned by US pension funds came from broad market exposure, something the funds could have achieved by indexing. However, the researchers found that active management played a much more significant role than market movements in explaining pension funds’ returns in hedge funds and other alternative asset classes.

DEFINITIONS OF ALPHA AND BETA ARE CHANGING

[A.L.] I’d like to expand on what Nicolas has just said. As “beta” expands to encompass not just traditional, capitalisation-weighted market indices but also smart beta indices, which embed different investment strategies and risk factor exposures, “alpha” may also change its definition.

There is likely to be much greater scrutiny of the extent to which active managers truly add value, for example by studies focusing on managers’ “active share” against their performance benchmarks. And those benchmarks may be more tailored to managers’ individual styles. For example, if an active manager specialises in small-cap US value stocks, why not measure his performance against the relevant smart beta index, rather than against the broad market?

PASSIVES AND ALTERNATIVES ARE COMPLEMENTARY

[N.G] We often see passive and active management described as being in a fight for investors’ assets. I don’t think this is the right way of viewing things. Instead, index-based portfolio solutions (such as passive funds and ETFs) and truly active funds (in the form of alternatives) should be seen as complementary. In fact, in Lyxor’s view these portfolio approaches can by themselves provide a full solution for the average investor.

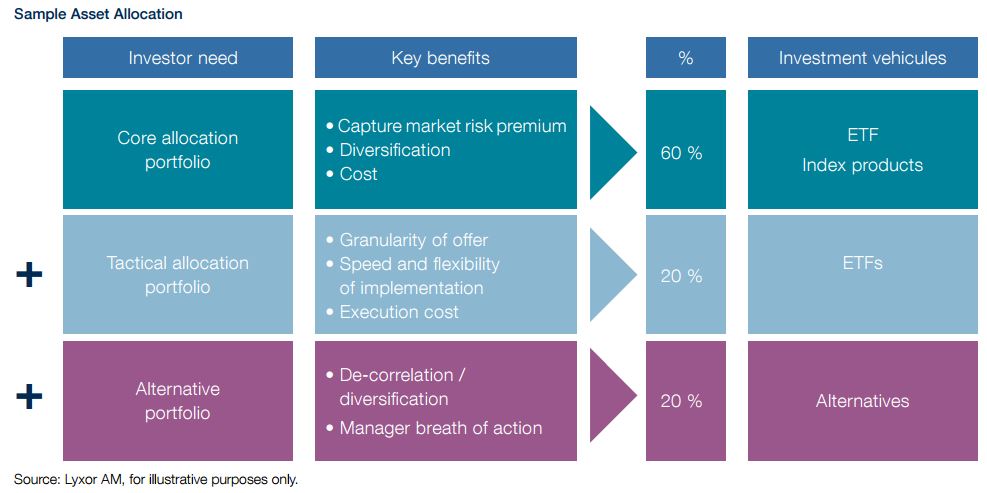

Broad-based ETFs and other index products, typically tracking capitalisation-weighted indices, are well-suited to the portfolio core. They capture market risk premia and offer effective diversification at low cost.

ETFs are ideal for tactical asset allocation, since they offer high granularity of exposures, ease of implementation and low execution costs. Such tactical positions could include ETFs based on strategy and factor indices.

Alternative assets can then form the active part of the portfolio, based on the principle of uncorrelated exposures and unconstrained investment mandates.

A typical portfolio could be split 60/20/20 between core ETFs and index products, tactical exposures using ETFs and the active component, represented by alternatives.

COMBINING ACTIVE AND PASSIVE

[N.G] Asset allocation approaches are evolving to take into account the broadening range of low-cost, index-based solutions and the growing evidence that alternatives are the true form of active management. We believe that combining traditional beta, smart beta and alternatives in a portfolio provides a very effective and powerful solution for the average investor.

Arnaud Llinas , Nicolas Gaussel , April 2015

Article also available in :

English ![]() |

français

|

français ![]()

Footnotes

[1] http://www.lyxor.com/fileadmin/PDF/... FACTOR_RONCALLI_GB.pdf

[2] According to a study by Cliffwater and Lyxor AM.

[3] https://www.regjeringen.no/globalas... eksterne-rapporter-og-brev/ags-report.pdf

Focus

Opinion Psychology and smart beta

‘Smart beta’ sounds like an oxymoron. How smart can it be to continue using the same strategy in such fickle markets? A portfolio manager calling on all his skills (‘alpha’) in analysing market environments (the source of ‘beta’) should be able to outperform an unchanged (...)

Releases

Analysis

Advertising

Zoom

-

European crisis

-

Hidden assets

-

Multi-asset funds

-

Smart Beta

-

Strategies on divide

-

Alternative Risk

-

Infrastructure

-

China

-

Gestion Obligataire

-

Gestion Action

-

ETF Actions américain

-

Actions Thématiques

-

Special Investisseme

-

Économie bleue : (...)

-

Les thématiques (...)

-

L’IMPACT CHEZ CPR

-

ACTIONS THÉMATIQUES

-

La voie vers l’écono

-

Comment les investis

-

Assurer l’avenir (...)

-

Forex

-

Mory Doré’s column

-

Éclairages Économique

-

Solvency II

-

Managed Accounts

-

Les Derivés Total

-

Contrats à terme (...)

-

France’s debt

-

Recherche Quantitati

-

The french marketpla

-

RSS Feeds

| News Feed | |

| Jobs & Internships | |

| Trainings |

|

|

Site | English | Francais | Mobile | Facebook | Twitter |